All Categories

Featured

Table of Contents

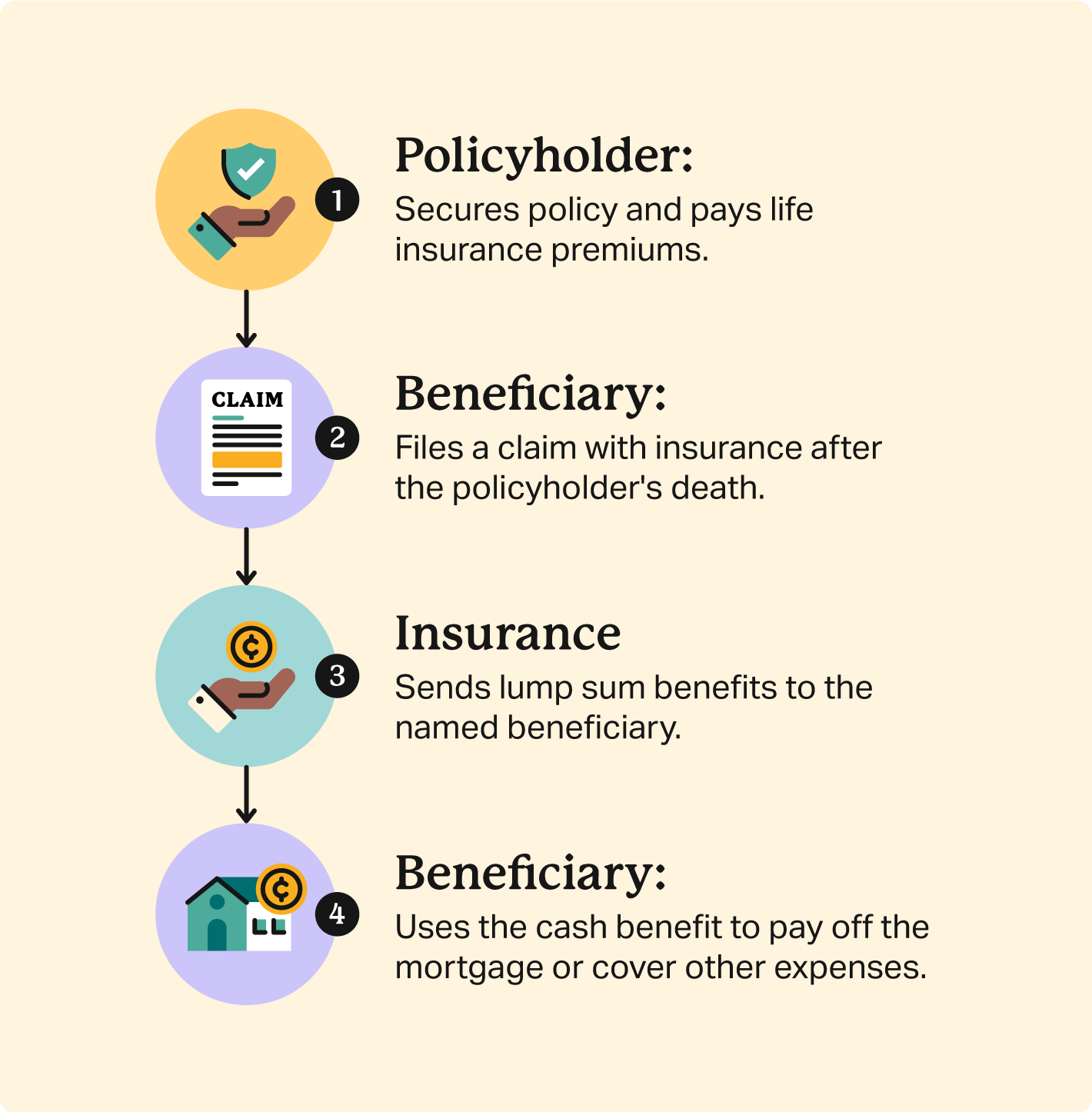

Another possibility is if the deceased had a current life insurance policy policy. In such cases, the designated recipient may receive the life insurance earnings and use all or a part of it to pay off the home mortgage, permitting them to stay in the home. what does mortgage protection insurance cover. For individuals who have a reverse home loan, which enables people aged 55 and above to obtain a home mortgage finance based on their home equity, the car loan passion accrues over time

Throughout the residency in the home, no repayments are called for. It is necessary for people to meticulously intend and take into consideration these variables when it comes to home loans in Canada and their influence on the estate and heirs. Seeking assistance from legal and financial experts can aid guarantee a smooth change and correct handling of the home mortgage after the property owner's death.

It is essential to understand the available choices to make certain the home loan is correctly dealt with. After the death of a house owner, there are several choices for home mortgage settlement that depend upon numerous factors, consisting of the terms of the home mortgage, the deceased's estate planning, and the dreams of the successors. Here are some usual options:: If numerous successors want to think the mortgage, they can come to be co-borrowers and proceed making the home loan payments.

This alternative can supply a clean resolution to the home mortgage and distribute the continuing to be funds amongst the heirs.: If the deceased had an existing life insurance coverage policy, the assigned beneficiary may obtain the life insurance policy profits and utilize them to settle the home loan (quicken loans mortgage protection insurance). This can allow the beneficiary to remain in the home without the problem of the home loan

If nobody remains to make home loan settlements after the home owner's fatality, the home mortgage financial institution has the right to seize on the home. The effect of repossession can vary depending on the circumstance. If a beneficiary is named yet does not sell the house or make the home mortgage settlements, the home mortgage servicer can start a transfer of ownership, and the foreclosure could badly damage the non-paying heir's credit.In situations where a house owner dies without a will or count on, the courts will certainly assign an executor of the estate, normally a close living family member, to disperse the assets and responsibilities.

Mortgage Protection Plan Vs Life Insurance

Home mortgage security insurance coverage (MPI) is a form of life insurance policy that is especially designed for individuals who intend to make sure their home mortgage is paid if they pass away or come to be disabled. Often this sort of policy is called mortgage settlement defense insurance. The MPI process is easy. When you pass away, the insurance coverage earnings are paid directly to your home loan business.

When a financial institution owns the big majority of your home, they are liable if something takes place to you and you can no much longer make settlements. PMI covers their threat in case of a repossession on your home (compare the market mortgage life insurance). On the other hand, MPI covers your risk in case you can no much longer make payments on your home

The amount of MPI you require will differ depending on your one-of-a-kind situation. Some variables you ought to take right into account when taking into consideration MPI are: Your age Your health and wellness Your economic circumstance and sources Other types of insurance policy that you have Some people might think that if they currently have $200,000 on their home mortgage that they need to get a $200,000 MPI plan.

When Do You Have To Have Mortgage Insurance

The inquiries individuals have concerning whether or not MPI is worth it or not are the exact same concerns they have regarding purchasing various other kinds of insurance coverage in general. For the majority of people, a home is our solitary biggest financial obligation.

The mix of anxiety, grief and altering family members dynamics can create also the most effective intentioned individuals to make expensive blunders. mortgage protection companies. MPI solves that trouble. The worth of the MPI policy is straight connected to the balance of your home loan, and insurance policy profits are paid straight to the financial institution to look after the staying balance

And the largest and most difficult economic concern encountering the surviving relative is dealt with promptly. If you have wellness problems that have or will certainly produce problems for you being accepted for regular life insurance, such as term or entire life, MPI can be an exceptional choice for you. Typically, home loan security insurance plan do not need medical examinations.

Historically, the amount of insurance protection on MPI plans dropped as the equilibrium on a mortgage was minimized. Today, the coverage on many MPI plans will stay at the very same degree you bought originally. If your original home loan was $150,000 and you bought $150,000 of home mortgage protection life insurance, your recipients will certainly now get $150,000 no matter how a lot you owe on your home loan.

If you desire to settle your mortgage early, some insurance coverage companies will allow you to transform your MPI plan to another kind of life insurance policy. This is just one of the concerns you might wish to address in advance if you are considering repaying your home early. Costs for home loan security insurance will vary based on a number of things.

Mortgage Care Insurance

An additional aspect that will certainly influence the costs amount is if you get an MPI policy that supplies insurance coverage for both you and your partner, providing benefits when either among you dies or comes to be handicapped. Realize that some companies might require your plan to be editioned if you re-finance your home, yet that's normally just the situation if you acquired a policy that pays out just the balance left on your home loan.

Therefore, what it covers is really slim and plainly defined, relying on the alternatives you pick for your particular policy. Self-explanatory. If you pass away, your home loan is settled. With today's plans, the value may exceed what is owed, so you can see an added payout that might be utilized for any undefined usage.

For home loan defense insurance, these forms of extra insurance coverage are added on to plans and are known as living advantage riders. They enable plan holders to touch right into their mortgage protection advantages without passing away.

For instances of, this is usually now a cost-free living advantage provided by a lot of firms, yet each company specifies benefit payments in a different way. This covers ailments such as cancer cells, kidney failure, heart assaults, strokes, mind damage and others. mortgage insurance in the event of death. Companies typically pay in a swelling amount depending on the insured's age and seriousness of the illness

In many cases, if you make use of 100% of the allowable funds, after that you made use of 100% of the policy fatality benefit value. Unlike most life insurance policy policies, getting MPI does not need a medical test a lot of the time. It is marketed without underwriting. This implies if you can not get term life insurance as a result of an illness, an assured concern home mortgage defense insurance coverage policy might be your best option.

Preferably, these ought to be individuals you understand and trust fund who will provide you the very best guidance for your circumstance. Regardless of that you make a decision to check out a policy with, you ought to always look around, due to the fact that you do have alternatives - loan insurance policy. Occasionally, unintended death insurance policy is a far better fit. If you do not get approved for term life insurance, after that unintentional death insurance may make more feeling because it's assurance concern and means you will not be subject to medical tests or underwriting.

Is Mortgage Insurance Paid In Arrears

Make certain it covers all costs related to your home loan, consisting of passion and repayments. Ask just how swiftly the policy will certainly be paid out if and when the main earnings earner passes away.

{kind=link}

Table of Contents

Latest Posts

Life Funeral Insurance

Funeral Cost Insurance

Funeral Life Insurance Policy

More

Latest Posts

Life Funeral Insurance

Funeral Cost Insurance

Funeral Life Insurance Policy